< Acquisition International Awards > [Certificate]

We are the first appraisal/valuation firm in Japan which won the AI Award.

This is one of the most prestigious awards for business, legal, financial, and investment

advisers in the world.

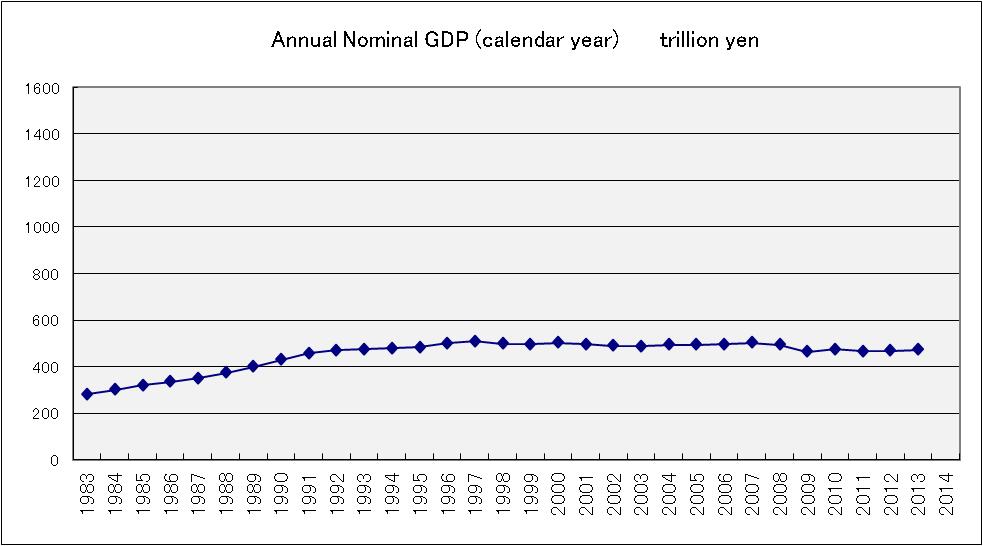

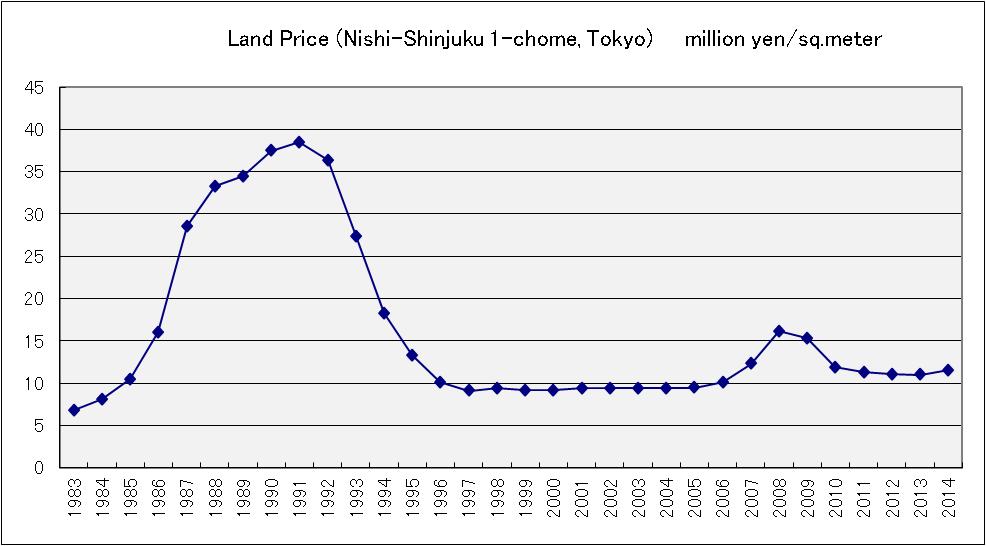

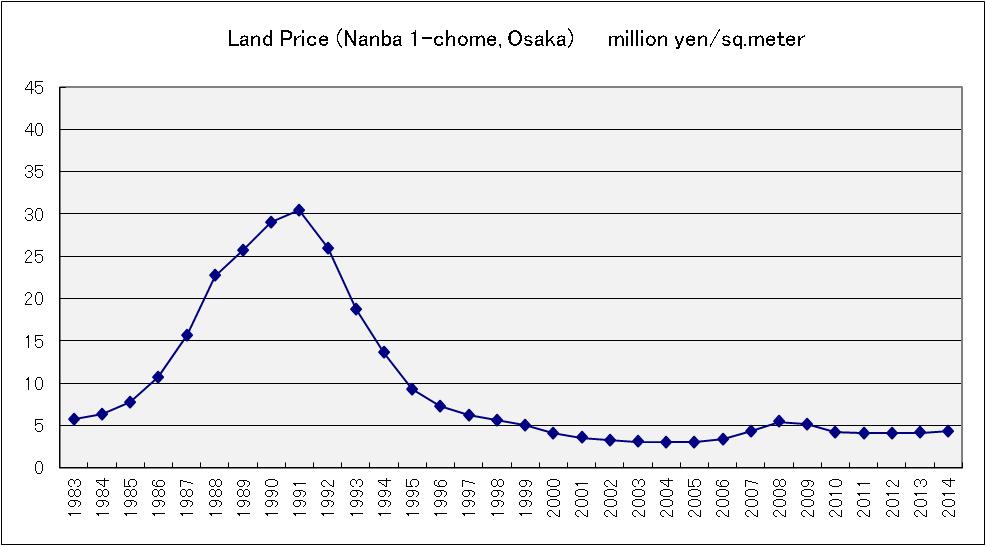

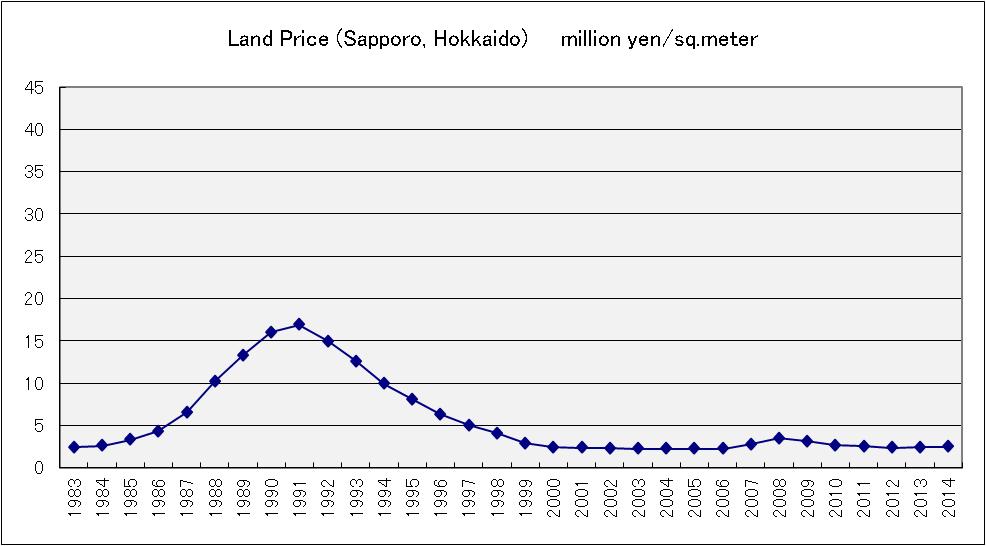

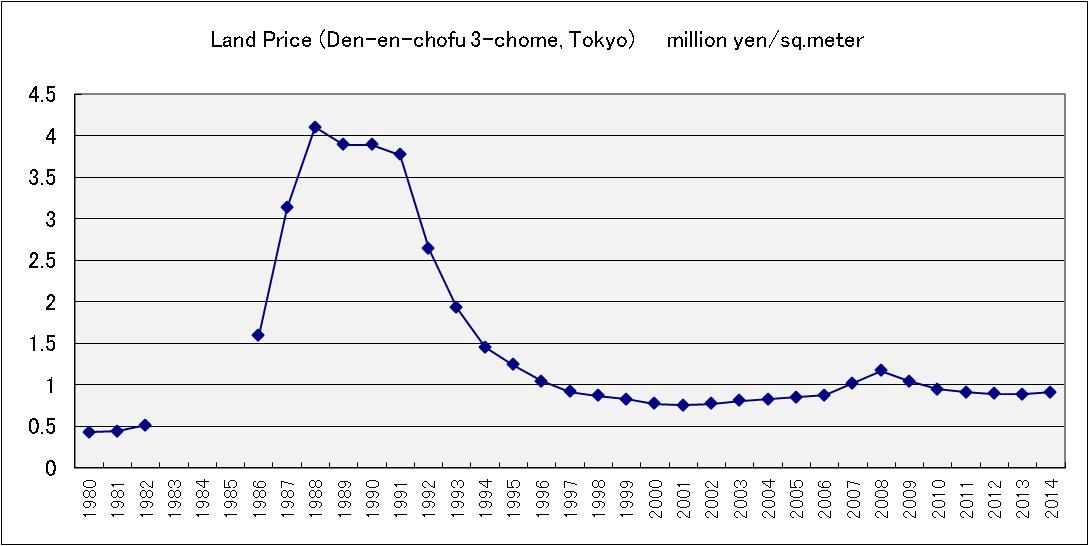

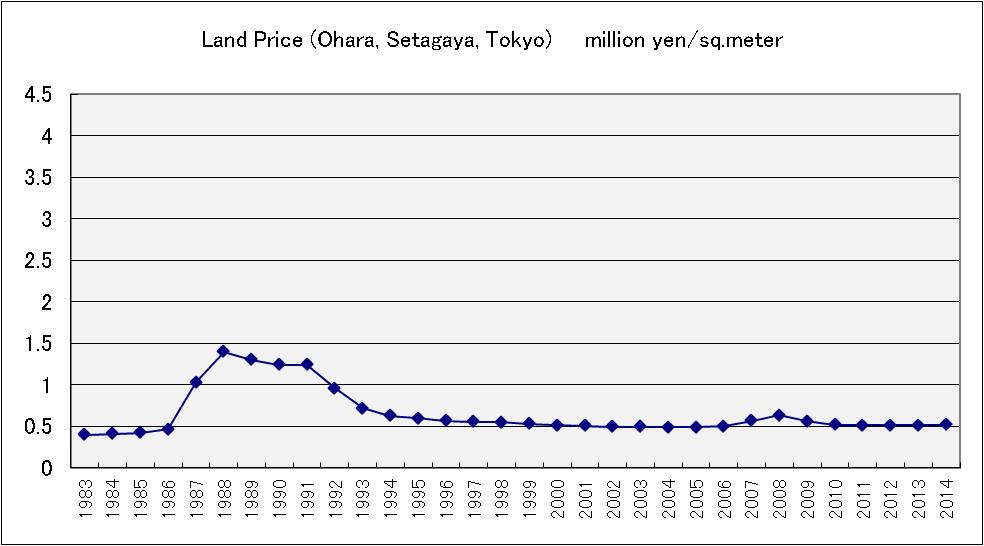

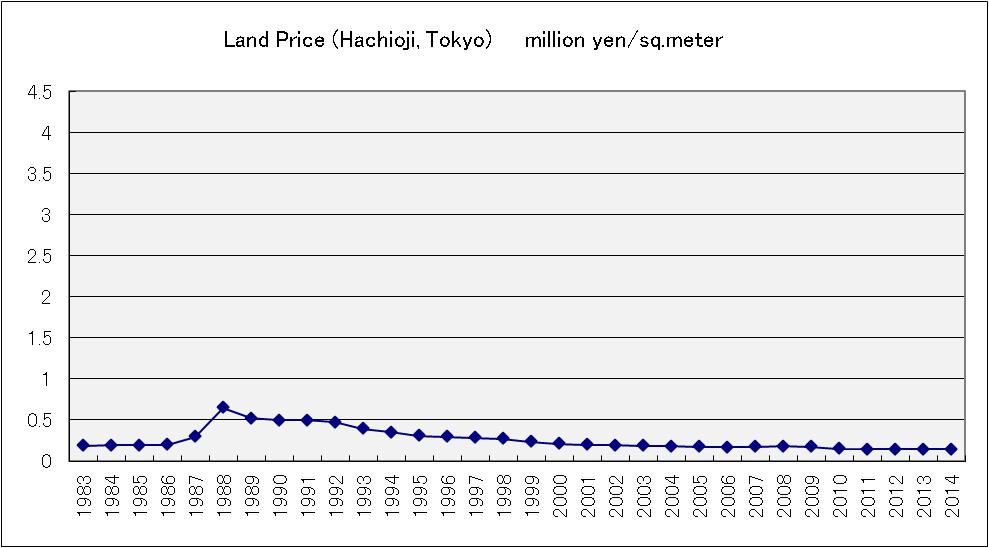

"What Caused the Bubble?" on this website was taken as a supporting evidence by AI

in the assessment process.